The Price of Not Knowing the Price

Health insurance costs are climbing again in 2026 and the ACA subsidy cliff is pushing millions to go without coverage. Here's why paying cash can beat insurance, and how SumHealth's free cash price checker puts real hospital prices in patients' hands.

There is a particular kind of silence that falls over a kitchen table in October, when the renewal notice arrives. It is not the silence of surprise. It is the silence of people doing math they already know the answer to.

Here is the math.

Employer sponsored health insurance is set to climb again in 2026, with total health benefit costs per employee expected to rise roughly 6.5 to 6.7 percent. That is the steepest jump in fifteen years, and the fourth straight year of increases well above the decade long average of about 3 percent. Mercer, which surveys more than 1,700 U.S. employers every year, called it the highest cost increase since 2010. Employees are expected to see their own paycheck deductions rise 6 to 7 percent as a result, on top of higher deductibles many employers are adding to soften the blow to their own budgets.

That is the “good” news. That is the news for people whose employer still writes most of the check.

For everyone else, the story is worse.

On the Affordable Care Act marketplace, where 24 million Americans found coverage, many for the first time in their working lives, premiums jumped by more than 20 percent on average for 2026. The Commonwealth Fund called it an aberration, and the driver was clear: the expiration of enhanced federal subsidies that had kept costs artificially low since 2021. For the roughly 22 million people who relied on those enhanced subsidies, the math is almost cruel. KFF estimates that average net premium payments for subsidized enrollees more than doubled, and the Urban Institute puts the jump even more starkly for lower income enrollees, from about $169 a year to over $900 under standard subsidies.

Economists at the Urban Institute and the Congressional Budget Office have tried to put a number on what happens next. Their estimates converge on an uncomfortable range. Somewhere between 4 and 5 million Americans are expected to become uninsured in 2026 alone, as a direct result of the subsidy cliff. That is on top of the 27.1 million people who were already uninsured as of the most recent Census data, a figure that had already ticked upward for the first time in years, largely due to Medicaid unwinding.

Early 2026 enrollment data bears this out. Effectuated ACA marketplace enrollment has fallen to somewhere between 16.5 and 17.5 million people, down from 22.3 million in 2025. That is the first year over year decline in marketplace enrollment since 2020, and it arrived right on schedule with the subsidy cliff.

Young, healthy adults are dropping out first, and that is its own kind of warning. When the people least likely to file a claim leave the risk pool, the people who remain get sicker on average, and premiums rise again to compensate. Health economists have started calling this cycle, without much affection, a death spiral. The Urban Institute found that adults nineteen to thirty four years old account for nearly half of the projected increase in uninsured Americans this year.

So here is where the country finds itself. Millions of people are being priced out of a system that was built, however imperfectly, on the idea that everyone would eventually be inside it. They are not becoming less sick. They are not needing care less often. They are simply choosing, or being forced, to face that care without a card in their wallet that makes the number smaller.

Which brings us to a fact that surprises almost everyone the first time they hear it. Paying cash can be the better deal.

A peer reviewed analysis published in the Journal of General Internal Medicine looked at common, shoppable hospital services and found that the discounted cash price was lower than or equal to the median commercial insurance negotiated price 47 percent of the time. Nearly a coin flip, and often a better one for the patient holding cash. The effect was strongest at nonprofit and government hospitals, in communities with higher uninsured rates, and outside major metro areas, which happen to be exactly the places where the newly uninsured are most likely to live. Independent labs and imaging centers tell a similar story. A comprehensive metabolic panel that runs $100 to $250 through insurance can often be had for $15 to $40 in cash. An MRI at an independent facility can cost a fraction of the hospital rate for the same scan.

None of this is a secret, exactly. It is federal law. Hospitals have been required to publish their prices since 2021, and a newer CMS rule tightening those requirements took effect this year, with enforcement starting April 1. But compliance has been spotty. One federal review found that barely a third of hospitals fully met the standard. And even where the data exists, it lives in sprawling machine readable files built for insurance actuaries, not for a person trying to figure out what a shoulder MRI costs on a Tuesday afternoon. NPR reported earlier this year that the transparency data, four years after the rule took effect, is mostly being used by health systems and insurers to benchmark each other’s contracts, not by patients trying to shop for care.

That gap, between prices that legally must be public and prices a human being can actually find and use, is the gap we built our tool to close.

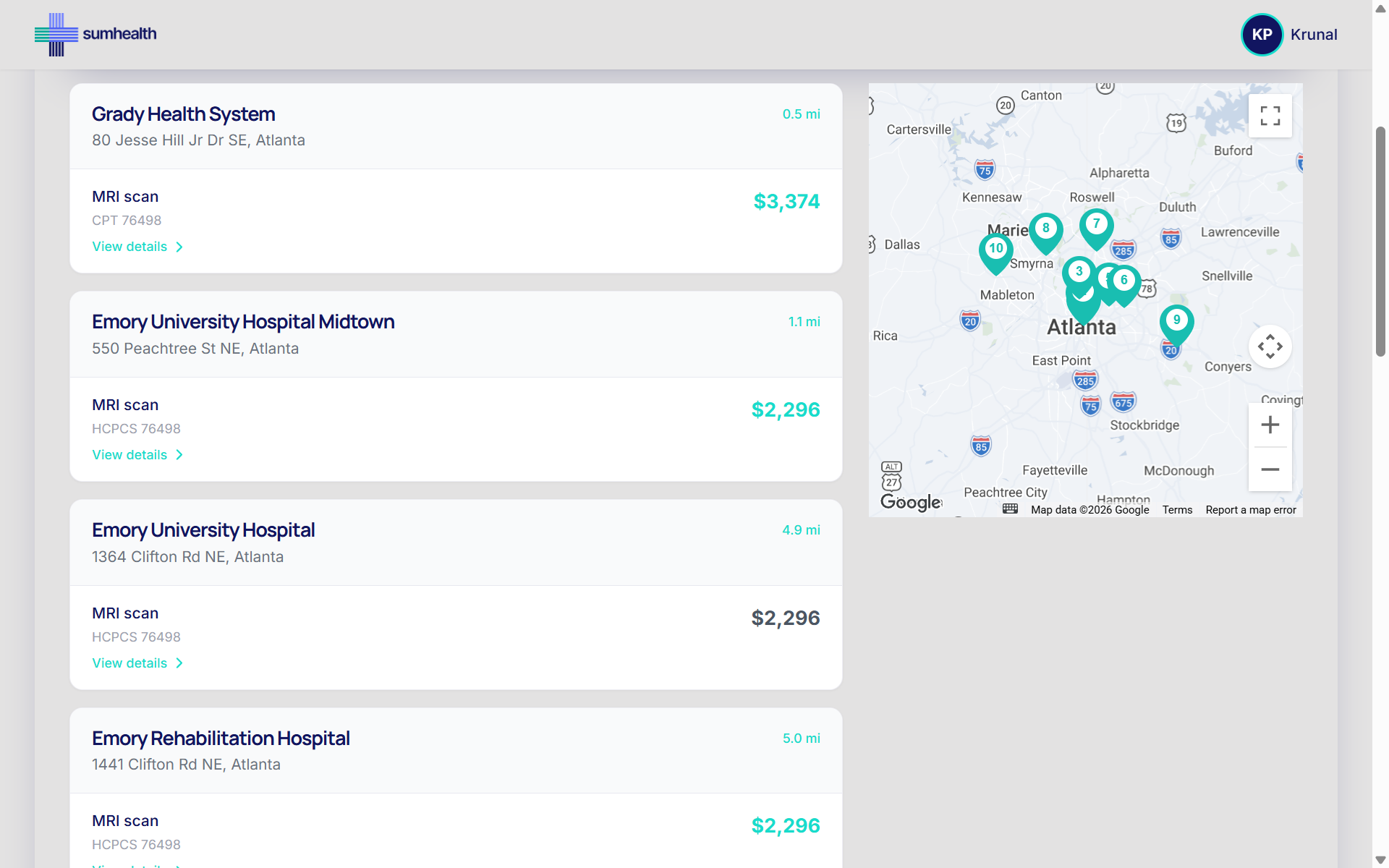

The Free Hospital Cash Price Checker, at search.sumhealth.org, lets anyone look up real cash prices for medical procedures at hospitals near them. Free to sign up. No insurance card. No cost. Type in a procedure, an MRI, a colonoscopy, an ER visit, a routine bloodwork panel, and see what hospitals in your area actually charge self pay patients, side by side. It takes the same information buried in those chargemaster files and puts it in front of the person who needs it most: the one standing at the counter, phone in hand, trying to decide whether they can afford to be seen today.

We built it because we kept running into the same story, told a hundred different ways by a hundred different people. Someone loses a job and loses coverage with it. Someone’s employer switches to a high deductible plan and the deductible might as well be a wall. Someone ages off a parent’s policy at twenty six and decides, for now, to go without. Someone simply cannot make the ACA math work anymore, not this year, not with premiums where they landed. In every version of that story, the person still gets sick sometimes. They still need an X ray, or a scan, or stitches. And in every version of that story, the first question they ask isn’t “what’s covered.” It’s “what does this cost, and can I afford to find out.”

There is a version of the healthcare debate that lives entirely in Washington: in reconciliation bills, in CBO scores, in the open question of whether Congress restores a subsidy before the next open enrollment period. That debate matters enormously, and it is nowhere near settled. It will keep being fought over for years, and the outcome will shape how many Americans have coverage at all.

But there is another version of this story that lives at kitchen tables, where the renewal notice already arrived, the decision already got made, and insurance already is not part of the plan for this year. For those people, the most useful thing anyone can offer is not a policy position. It’s a number. A real one, in advance, so the choice about whether to get care is never confused with the choice about whether to know what it costs.

That is what the Free Hospital Cash Price Checker is for. It is free because the price of not knowing shouldn’t be one more thing added to the bill.

Sources: Mercer National Survey of Employer Sponsored Health Plans, Commonwealth Fund, Urban Institute, KFF, U.S. Census Bureau, Congressional Budget Office, Journal of General Internal Medicine, NPR/KFF Health News.

Ready to see the data for yourself?

SumHealth processes hospital and payer MRF rate data nationwide so you don't have to. Talk to our team about how our platform can power your pricing strategy.

Schedule a Demo